DeFi Yields, Demystified

DeFi Yields, Demystified

Let's breakdown where these astronomical yields in DeFi actually come from, the mechanisms through which they are generated and if these yields are sustainable in the long run

Hi Friends 👋🏼

If you've been hanging around the DeFi space over the last 12 months, you would have probably noticed that the space has moved on from the early days of deciding WHAT assets to hold. Now the questions lies in WHERE to hold these assets. In the last 12 months, you would have seen different platforms offering mind-blowing yields on your assets, anywhere from your measly 10% , to 10,000% or even an insane 100,000% APR.

While DeFi degens might look at these yields and lick their lips in anticipation, regular people instead express skepticism and suspicion. How are these platforms creating these returns out of thin air? This MUST be a scam? There MUST be catch! These concerns are understandable considering how out-of-whack they seem when compared your traditional finance (TradFi) savings account where getting 1% is already cause for celebration.

Skepticism is healthy but it’s important that the skepticism is followed up with some research to validate it. Hence, my goal here is to provide you the research/facts and demystify DeFi yields. We'll dive into what yield actually is, the common mechanisms to generate yield, where the yields come from and whether these yields are sustainable in the long run.

Don’t forget to join you a bunch of other smart and curious folks and learn more from my deep dives into all things Technology, Web3 and the Ownership Economy.

Let's dive right in👇🏼

Note: To ensure this article doesn’t evolve into a thesis , I will be ignoring yield that can come from the increase in the value of the assets that you hold (e.g. BTC price increasing from $2,000 → $50,000 kinda thing) since that is pretty well understood. I’m also ignoring derivatives (options, leverage tokens etc) since in DeFi, I count those as bonus yield as you can already get astronomical yields without derivatives. I will focus on the more "passive-ish" yield that most folks have adopted in the DeFi space.

What is Yield?

Calculating Yield

Before we go any further, we need to first have an aligned definition of what we are about to discuss.

Yield.

Yield refers your return on capital invested over a particular period of time (usually a year). It is expressed as a percentage based on the invested or principal amount.

Say you bought 1 hypothetical Google stock ($GOOG) for a 100 dollars, and after a year it is worth $120. The stock also pays you a $2 dividend per share annually. Your yield refers to the appreciation in the share price + any dividends paid, divided by the original price of the stock. The yield for this example would be:

($20 + 2) / $100 = 0.22 or 22%In DeFi today, this yield is promised by various platforms in exchange for a service or staking:

E.g. : Provide your DogCoin Tokens that you had bought, as liquidity to a crypto platform and earn 30% yield for doing so for a year.

Very similar to the concept of buying a $GOOG stock and seeing the asset value growth + receiving regular dividends, just with a different source this “dividend”.

When people quote yield APYs in the DeFi world, it is often assuming a stable base asset value and the yield comes from the “dividend” side where the application / protocol is disbursing assets to you, driving your returns.

In DeFi however, that the yield you are receiving from the protocols can be entirely, or at least partially in the form of the protocol's governance tokens, not stable USD. These tokens can be volatile and can significantly affect your real yield. A common mistake among many newer DeFi investors is to think about their potential yield in dollars and not considering that the yield APR quoted refers to number of tokens, not their dollar value. Most also do not consider the volatile nature of their principal investment, instead assuming it would be stable.

This example should illustrate the point:

Let's say you start with 100 DogCoin Tokens ($DCT) currently priced at $1 and you stake it on a protocol offering 50% yield. As mentioned, the yield % refers to the no. of tokens you earn over a year, so you would end up with a 150 $DCT tokens not $150 dollars worth of $DCT. YAY! But, now the price of each $DCT token has dropped to $0.20, and your stake which started being worth $100 is now worth $30. In dollar terms, you have lost money despite putting your assets on a platform offering you 50% yield. This might still be an outcome you are happy with, depending if your goal was to make returns in dollars or to grow your $DCT stack.

APR vs APY

One should also be crucially aware of how yield is quoted. Different platforms vary between using APRs vs APYs which can make it difficult to make an apples-to-apples comparison.

APR refers to the Annual Percentage Rate: The percentage of interest an investor / depositor will earn over a year. For example, if you invested$100 at an APR of 10%, you would profit $10 at the end of the year (100 x 0.10)

APY refers to Annual Percentage Yield. It is similar to APR, except that it accounts for the compounding of interest (i.e. reinvestment of dividends)

Different figures may work better for different protocols depending on how they work. As an investor, you should always be aware of what the figure displayed refers to so you can make the right investment decisions.

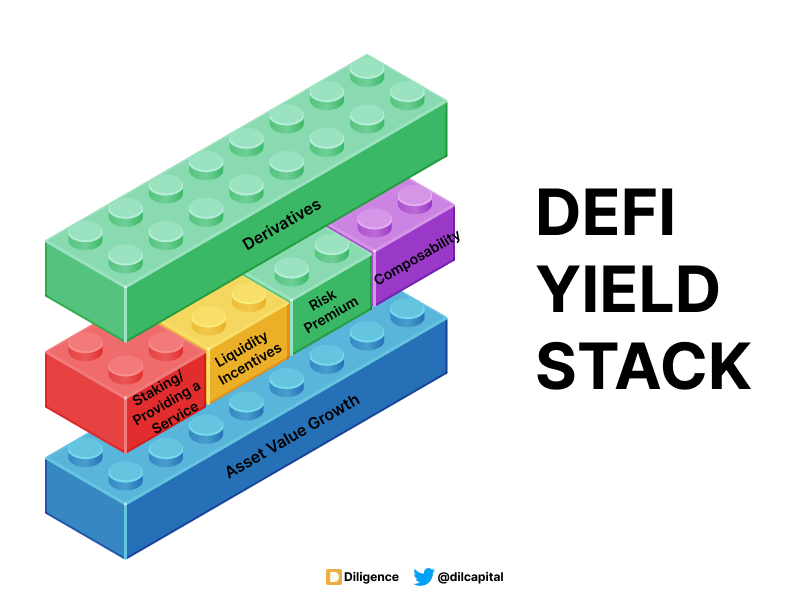

The DeFi Yield Stack

Before we go any deeper, I think it’s probably useful to build a mental model of how to think about yield in DeFi. I like to look at yield as being being made up of an additive set of blocks, where with each block contributes to your total real yield.

In my model, the blocks are not fixed in any particular order.

Just like in TradFi, derivatives can help you to both mitigate the downside but also help you achieve outsized returns across all areas of the stack.

As mentioned earlier, in this article, we won’t be touching on Asset Value Growth or Derivatives since both work very similarly to TradFi and are pretty well understood.

❌ Asset Value Growth

❌ Derivatives

✅ Base DeFi Yield

✅ Liquidity Incentives

✅ Composability

✅ Risk Premium

Underlying Mechanisms of Generating Yield

There are fundamentally 2 underlying sources / mechanisms from which primary yield can be earned from:

Providing a Service

This can mean a lot of different things but today, usually refers to helping supply liquidity to different liquidity pools and lending pools to service borrow demand

Staking

While the term staking is used very loosely today to describe any process where you lock up you assets in exchange for rewards, we will talk about the most common form of staking, staking as part of Proof-of-Stake.

Providing a Service

A. Servicing Borrowing Demand

This is probably the most intuitive source of yield in DeFi. The natural demand to borrow funds exists in very capital market. Retail folk like us might need to borrow funds to buy a new car, a business might need working capital to buy building materials and a financial institution might want additional funds to reinvest in assets that they are very bullish on. This natural demand to borrow assets automatically creates a market for borrowers and lenders and enables price discovery for loans. In the TradFi world, banks usually perform this service, lending out money off your deposits. The banks then keep most of the interest they make off the loan, giving you only the scraps. For a decentralised lending platform, >70% of the lending interest charged, ends up with the lender.

In DeFi, 99% of loans are over-collateralized and come with a pre-defined loan-to-value ratios (LTV). LTV defines how much users can borrow based on the value of collateral they deposit.

For example, if you deposit 5 BTC worth $20,000 each as collateral and the BTC/USDC lending pool has an LTV of 50%, you can with draw up to $50,000 worth of $USDC. On the supply side, users can deposit $USDC into the same liquidity pool and earn a yield from providing the lending liquidity. The platform might charge the borrower a 5% interest and give 4% as a reward to liquidity providers. The more exotic, illiquid or in-demand the asset, the higher the interest rates and rewards tend to be.

A frequent question that arises is why are borrowers in crypto willing to pay such a high interest rate (in the excess of 4%-20%) to get access to these funds?

This is likely a function of market inefficiencies today between the supply and demand of different assets. In addition, these lending platforms have to set these supply rates such that they are also able to incentivise a user to deposit out their assets while at the same time ensure the interest rates are still attractive to a borrower. Another likely factor has to do more with the eventual return a borrower can attain with the funds he has borrowed. Especially in crypto, returns of 100-1000%, especially with leverage, are not uncommon which increases the tolerance towards what might be a 10% borrowing APR.

Another common question touches on the over-collateralisation of loans in crypto and why someone would deposit $100,000 worth of BTC only to be able to borrow $60,000 USD (if the LTV is 60%).

The brief answer here is that there is a large enough corpus of people who believe that the digital assets that they own will retail or appreciate in value, but at the same time, they need liquidity to fund other investments or to do some real world shit. These folks do not want to sell their asset to access the liquidity and hence being able to borrow against these valuable, appreciating assets alles them to access liquidity but at the same time not miss out on the upside of their assets. This is similar to how gold loans work in india where i t is very common or even wealthy individuals borrowing against their homes or business.

B. DEXs / AMMs / Derivatives

Decentralised exchanges are one of the great innovations of DeFi. It combines mathematics with financial incentives and has become the a key piece of base DeFi infrastructure in the ecosystem. These DEXs don't work off an order book but instead depend on liquidity pools to facilitate the exchange of tokens.

You as a liquidity provider (LP), would deposit different a pair of tokens of equal value into a liquidity pool.

E.g. if $ETH was worth 2,000. and you wanted to deposit 5 $ETH into an ETH/USDC pool, you would pair that 5 $ETH with 10,000 $USDC. Hundreds of other LPs will also deposit into the same pool. These pools then facilitate the exchange between the $ETH and $USDC token for users who come to the exchange. The exchange rate is algorithmically determined according to a pre-defined formula. As an LP, you are rewarded for providing liquidity to the exchange and you are rewarded with a proportional amount of fees that that the trading pair generates. This trading fee is the yield that you generate from LP-ing.

Note: The 0.05% - 1% fee refers to the cut of each transaction not the interest APR of your deposited funds.

Other sources of demand for borrowing that have emerged include decentralized derivatives exchanges’ single asset vaults, Flash Loans, Shorting etc.

Staking

If you're looking for a relatively stress-free way to generate yield DeFi, staking is the option for you. When you stake your assets, you are basically locking up your assets in exchange for a financial reward. The "staking" that is most referred to is staking associated with protocols that adopt a Proof-of-Stake consensus mechanism. These includes blockchains like Solana, Polygon and once the merge is complete, Ethereum as well.

So how does staking with these protocols generate yield for users / stakers? The goal of Proof-of-Stake is similar to Proof-of-work in that its all about ensuring the security and integrity of the blockchain. Unlike PoW which relies on a network of miners running GPUs at full tilt for validation, PoS instead relies on validators who check the validity of transactions and ensure the blockchain runs as designed without needing specialised GPUs or computers. Validators don't do this work out of charity nor is there a guarantee that all the validators would be good actors who have the blockchain and its community's best interest at heart. This is where the whole PoS mechanism comes in. Lets take the example of Ethereum:

To be a validator, you have to stake at least 32 ETH.

As a validator, you receive rewards for actions that help the network reach consensus. This can include batching transactions into a new block or verifying the work of other validators. This reward is the yield that you earn from staking and is paid out in the protocol’s native token.

However, if you try to cheat the system, you are punished. The system will slash the funds and you will lose the ETH that you have staked.

This staking reward can easily be thought of as the fee that the network pays out to maintain its own security. These PoS blockchains generate the funds to payout this security fee through transaction fees and / or a pre-determined inflation of their token supply. That is the yield you receive for staking.

Proof-of Stake’s staking yield is often perceived as the risk-free rate of a blockchain. While nothing in crypto is 100% risk-free, this is seen as the least risky option as you are only likely to lose your funds if you're a malicious actor or if there is a wholesale collapse of the PoS blockchain. In the second case, this risk can be minimised by only staking on mature blockchains like Ethereum.

Liquidity is King in DeFi and How The Battle For Liquidity Drives Yields Up

To understand where these really mind-blowing yields really come from, we must first come to terms with the fact that for now, 1 think drives all things in DeFi: Liquidity.

Liquidity is king in DeFi.

Outside of a qualified team, an understanding of market needs and the ability to build a good product, liquidity is the lifeblood of every DeFi project. Liquidity affects asset prices, your ability to buy, sell, exchange an asset, and whether you can do so without drastically changing the asset price. Only with sufficient liquidity can you enable proper price discovery of an asset. Since everything in DeFi runs on tokens, this movement, pricing and exchange of assets is critical. Whether you are a decentralised exchange (e.g. Uniswap), a decentralised lending platform (e.g. Aave) or even a new play-to-earn game (e.g. ), liquidity makes or breaks you.

For example, Uniswap's DEX relies on liquidity pools which need to be deep for a high-functioning, low-slippage exchange that users will want to use. For a lending platform like Aave, you want deep liquidity in your lending pools so that users have a sufficient supply of assets to borrow from. And, a gamefi project like Mines of Dalarnia will want their $DAR token to be liquid and easily trade-able on different exchanges so users can easily buy and sell their tokens.

Whoever controls liquidity controls DeFi

- Joey Santoro

Liquidity is not something that is infinite, it is only available in limited amounts, especially so in DeFi. If liquidity providers decide to put their liquidity on one platform, it means that another platform is missing out on that volume.

Hence, there is strong incentive for these apps to attract liquidity to their applications or protocols, especially for new players trying to bootstrap from zero. Financial incentives are the strongest driver of behaviour, especially so in the hyper financialized DeFi world. It makes sense that these applications and platforms, choose to spend a portion of their treasury or fundraise to incentivise users by dishing out their own governance tokens, to attract liquidity their platforms. It is this need for liquidity which drove the behaviour or liquidity mining and liquidity incentive programs and the higher APRs in DeFi over the last 2 years.

If you're struggling to wrap your head around this, or think that this is some type of Ponzi where platforms are just paying to get users, you can simply think of liquidity incentives the same way you would think of early Customer Acquisition Costs (CAC) in the traditional startup world. The money spent on liquidity incentives is how these platforms attract initial liquidity, customers and suppliers. Just like any other company that you know and love.

So in summary for this segment, while a platform may already have a sound, profitable (for both the platform and its depositors) business model from which it can generate income, it may choose to deploy invested funds to reward users, drive up yields, to solve the cold start problem, or to just attract liquidity away from other platforms as a competitive strategy.

These 2 examples should make things more clear:

- Compound

Compound was the OG large player to popularise this liquidity mining behaviour. In 2020, the lending protocol announced that they would distribute their native $COMP tokens to all users who supplied liquidity or borrowed from the platform. The $COMP tokens were added as a booster on top of base supply yield.

E.g. : If the ETH / USDC lending pair had a yield of 4%, additional $COMP tokens might boost it to reward you with an additional 5% yield. Compound also strategically used the $COMP tokens to drive liquidity into different trading pair pools that might have been less popular but important to the success of compound.

Polygon

For a protocol to succeed, it needs a very liquid and active capital markets living on it. Polygon saw the importance of this and started a $40 million dollar liquidity mining program to drive liquidity onto the Aave Polygon Market. This is provided as rewards to lenders and borrowers on the Aave Polygon Lending Market. And, it boosts the yield for lending out your assets which attracts liquidity to be deposited into these pools.

In summary, when liquidity comes onto different platforms due to the high yields, it is often coming from people, institutions who are taking assets that were parked somewhere else and moving it to this new higher yield bearing platform. This is the very essence of the battle for liquidity and how it drives increased yields. One thing to keep in mind is that these yields are often boosted using the platform's native token. So while you might earn the the base returns in USDC/USDT or the deposited asset, something like a Compound would provide additional rewards in $COMP, Uniswap with $UNI and Polygon with $MATIC. This makes it much more complex to calculate one's actual yield as part of your yield comes in the form of a volatile asset.

There is also larger issues to be discussed around the mercenary nature of liquidity miners, who move from project to project sucking them dry of their liquidity incentives and moving on. However that is a discussion for another day but just put simply, the best minds in the world are looking for new solutions, check out Olympus DAO, pushing the Protocol-Owned-Liquidity model to Curve and Andre Cronje's pioneering "ve" model.

Composability

Composability is one of the core features of DeFi. Composability means that DeFi assets, DeFi apps are all (or at least mostly) interoperable. Strong token standards in the various ecosystems define a specific way of how tokens should behave and be interacted with. This allows third-parties to easily support, interact with and built applications around any token following that standard. In Ethereum, the ERC-20 standard was formalised in 2017 and is by far the most common type of token issued today. The NFT token standard, ERC-721 is probably a distant second. This is standards are also further enhanced by a fairly strong open-source culture in the space as well.

DeFi today has been the largest proving ground for composability in crypto. DeFi assets and protocols today are often referred to as “money legos”, implying the ease with which they can stack together or interoperate.

An example:

User decides to be a liquidity provider (LP) on Uniswap, so she deposits her ETH and USDC tokens into the ETH/USDC liquidity pool.

Once you have deposited the liquidity, Uniswap automatically gives you ERC-20 LP tokens that represent your share of funds in the pool. These are the tokens you would use to claim back the liquidity you have deposited

These LP tokens however are not just stuck in the Uniswap application - they can be used within other DeFi protocols. The Uniswap LP tokens can now be used as collateral in the lending protocol Aave.

Aave then gives you another token representing your lending position and you can see how this process can continue

While these examples clearly shows how these things interoperate, one important fact to remember is that Aave did not have to get permissions or information from Uniswap to decide to accept Uniswap LP tokens as collateral. Because Uniswap LP tokens follow the ERC-20 standard, Aave can consume these tokens the same way they would any other ERC-20 tokens.

How does this tie back to yield? Lets use another example:

User decides to stake her $ETH on Lido (a staking platform). Lido gives the user back stETH, representing her staking position in Lido

(earns A% for staking)

User now takes the stETH to the liquidity pool on Curve (a decentralised exchange). Curve gives you crvstETH representing your stake in the liquidity pool.

(earns B% for staking)You can take that crvstETH to Yearn , deposit it into a vault and receive rewards. Yearn returns you yvcrvstETH for your position in the vault.

(earns C% for vault)

Now you can see how instead of just earning A% yield, you can, through the interoperability of the different platforms and tokens, earn yield on 3 different platforms off the same principal invested.

Risk Premium

And lastly, just like everything else in life, high risks can result in high reward or ruin. When you are a liquidity provider for very uncorrelated assets or immature assets or you are staking on a brand new blockchain or protocol, you are often rewarded for doing so. You’re taking on risk, so the platforms ensure you are comensurately rewarded for doing so. High Risk = High APYs. However the opposite also applies. As these protocols, assets, applications become more mature, and prove themselves, the associated risk premium for participating slowly dissipates.

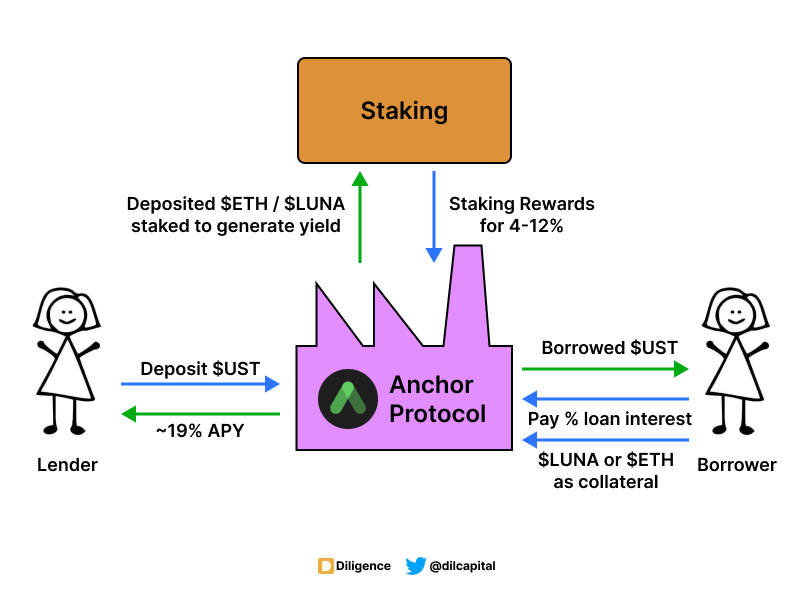

Anchor Protocol - Generating Yield across the Yield Stack

Anchor protocol is likely the most well-known stable and passive yield generating platform in DeFi. You basically deposit the UST algorithmic stablecoin into Anchor and earn a stable ~19% yield on your funds. While the returns might sound too good to be true, it is not. Anchor Protocol is a business like any other, it generates revenue but just like many high growth startups today, it chooses to not be profitable and instead spend its funds and revenue on growth.

Anchor’s generates revenue mainly via lending, similar to Aave. Users who want to access $UST stablecoin loans, come to Anchor, deposit $ETH or $LUNA and get $UST that they can they spend or re-invest. Anchor builds up this pool of $UST to lend out by incentivising deposits with a high and stable ~19% APY. To pay out this yield to lenders, Anchor charges an interest rate on $UST loans and also deploys the $ETH and $LUNA deposited as collateral to be staked (which generates a return on those assets for Anchor).

If you do the math, this 19% yield is actually not sustainable in the long run. We have already seen twice in recent times where the main benefactors of the Luna ecosystem have had to pump more funds into the system to ensure it can keep paying out the 19% +. This however, should not be seen as a bug. The protocol can actually choose to lower the yield to a much more sustainable and profitable 13% at anytime, but instead, had chosen to maintain the 19% for a long period of time. This is because their goal is to drive adoption of the $UST ecosystem and the larger LUNA ecosystem so this is just the cost of growth, similar to the funds spend on growth market and customer acquisition in a fast growing startup.

Its important to remembers that all these protocols are not static machines. Even the Anchor community has just approved a proposal to make the yield paid out semi-dynamic and dependent on the balance in the yield reserve. This will ensure the sustainability of the system.

DeFi Yield Stack

All to say, I hope that its become really clear how these different factors from the base yield mechanisms, to the battle for liquidity and the composability of DeFi, in combination with one another can offer investors such high yields in DeFi.

So Finally, Are These Yields Sustainable?

In short, the answer is no.

These yields will not last.

As the entire DeFi ecosystem continues to mature, market inefficiencies will get flattened out by new tools and more liquidity will enter the market, even-ing out the demand and supply for the most assets. It is almost certain that you will see yields collapse from the mind-blowing quadruple digit returns to something much more "normal".

This however, will take not happen immediately. Even the definition of ‘normal’ in DeFi will still be much more attractive compared to what you can get in the TradFi world. Protocols that offer a 120% yield may slowly taper it down to offering a 10% yield a year down the road, but that is still multiple times more attractive than your bank savings rate. Even just by simply staking a fairly safe asset like $ETH, post-merge most experts expect the staking rewards on $ETH to be >8%.

We also tend to underestimate how long these DAOs and protocols can continue to incentivise user behavior. Uniswap has a 2.2B treasury, Lido has 363M, Aave has 247M and the list goes on. These are some of the most well capitalised institutions with a lack of avenues to deploy their resources at the moment.

As the space matures, we should also expect to see more derivative products to appear in the decentralised finance space. These will also provide alternative options for participants with a higher appetite for risk to earn higher yields.

Wrap Up

So, if there's only one thing you take away from reading this, I hope it is that many of these applications and methods to generate yield on your assets are NOT scams. While just like any other gold rush, there will be unsavoury actors who will try to capitalise on our greed, you would be missing out on a lot of potential income and being early to the future of finance if you just paint every actor in the space with the same brush.

But reading explainers will only do so much. More than any other space, you have to Do it, to Believe it. If you can spare some change, buy some $ETH, create a Metamask wallet, have some fun and i’ll see you on the other side!

Thanks for reading! Don’t forget to share the article if you found it useful in any way. And hit me up on Twitter @dilcapital if you wanna make a new internet friend too!